![]()

Role of Supply Chains in Determining Farmers' Productivity and Consumer Prices

Chances are that the fruits and vegetables you ate today have been routed through one of the government-regulated wholesale markets after following a complex supply chain that starts with the farmers and involves a number of economic agents. District Lahore alone consumes approximately 8,000 tonnes of fresh produce daily, which travels to Lahore on trucks from remote rural locations across Pakistan. This may lead us to think that farming is a lucrative business; after all, everyone eats fruits and vegetables daily and the demand can only increase as the population rises.

Facts, however, point to a different reality. Suppose you spend PKR 50/kg today on potatoes. Only about PKR 20/kg of this amount is passed through to farmers. With this money, farmers must meet farming costs, sustain families, pay off liabilities and pay a fixed rent to the landowner (most farmers are landless tenants). Larger farmers enjoy economies that come with scale and are also less susceptible to credit constraints and the inability to access larger markets. Smaller and mid-sized farmers, on the other hand, find it very difficult to meet even basic household expenditures and are, therefore, reliant on various agents in the supply chain for their credit needs and accessing markets.

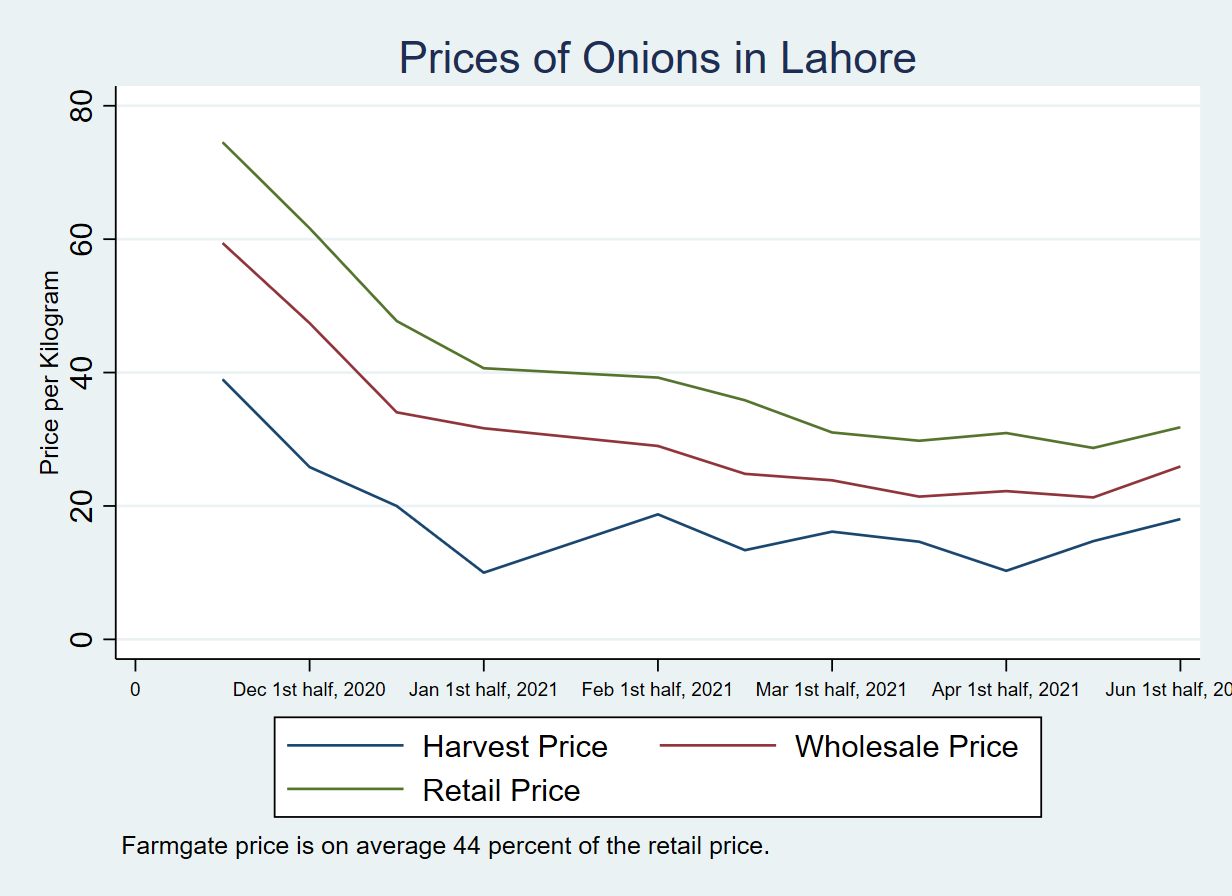

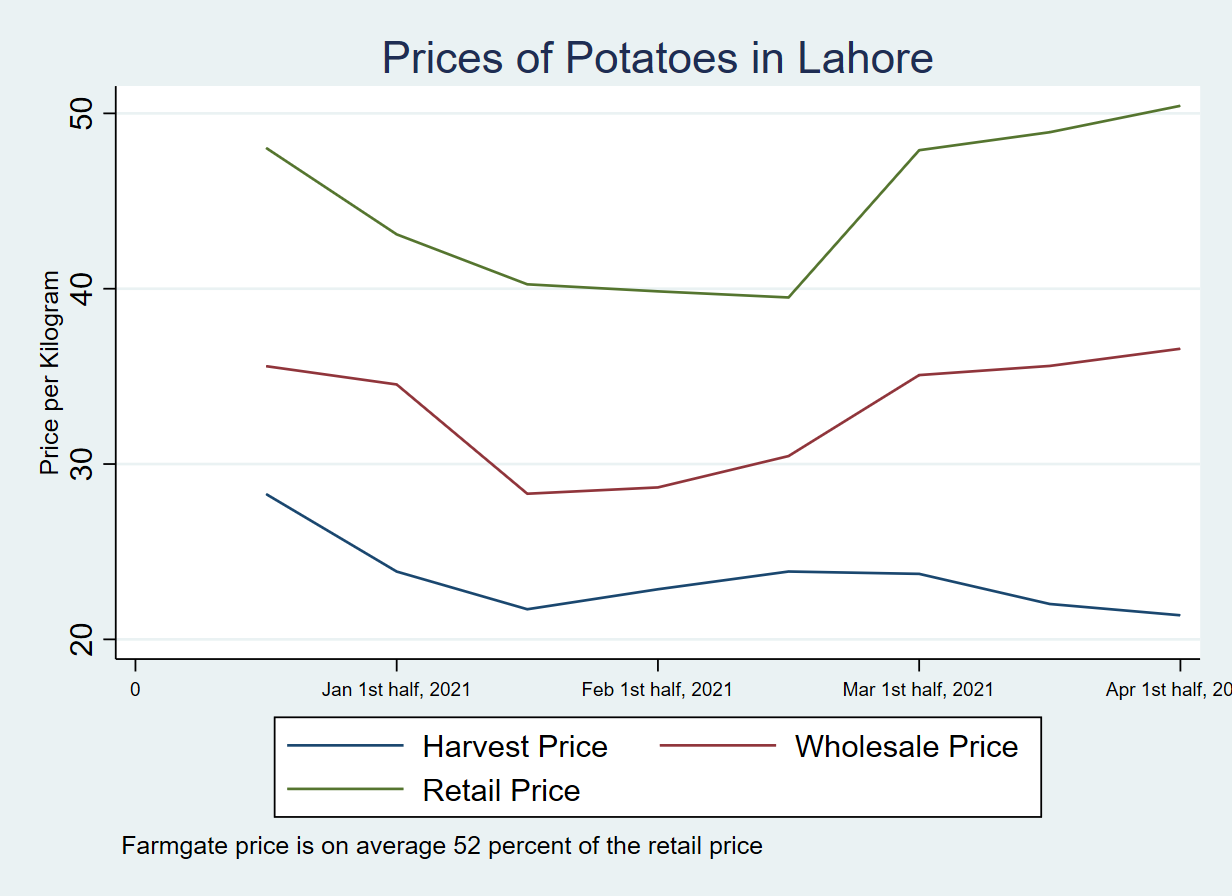

If you are wondering where the remaining PKR 30/kg go of the supposed amount, they are used to meet the costs of transport, labor, packaging, and profit margins of intermediaries (aartis, beoparis and phadias). This is true for the supply chain of nearly all fresh commodities. In Figures 1 and 2, we compare the prices received by the farmer (farmgate price) with auctioned prices (wholesale price) and the prices that consumers pay (retail price) for potatoes and onions in Lahore. It is shown that farmers on average receive about less than 50 percent of the price paid by the consumer for these items. This is extraordinary since there is no value addition of the produce from the farmgate to retail.

Figure 1: Price Comparison for Onions in Lahore

Source: Authors' own calculations. Data sources: Harvest Price Survey (Department of Agriculture, Punjab), Pakistan Bureau of Statistics, Agriculture Management Information System.

Figure 2: Price Comparison for Potatoes in Lahore

Source: Authors' own calculations. Data sources: Harvest Price Survey (Department of Agriculture, Punjab), Pakistan Bureau of Statistics, Agriculture Management Information System.

Why should we care if farmers are not getting enough returns while consumers are paying very high prices? This issue lies at the heart of both lower agricultural productivity and high food inflation in the country. The low pass-through to farmers implies that they do not have sufficient incentive to innovate and cultivate high-value products; instead, they cultivate low-value crops which have limited export potential. Consumers, on the other hand, are paying high prices due to the low price elasticity of agricultural produce and the presence of a large number of intermediaries in the supply chain. To understand the role of intermediaries, we need to understand how supply chains work in Pakistan.

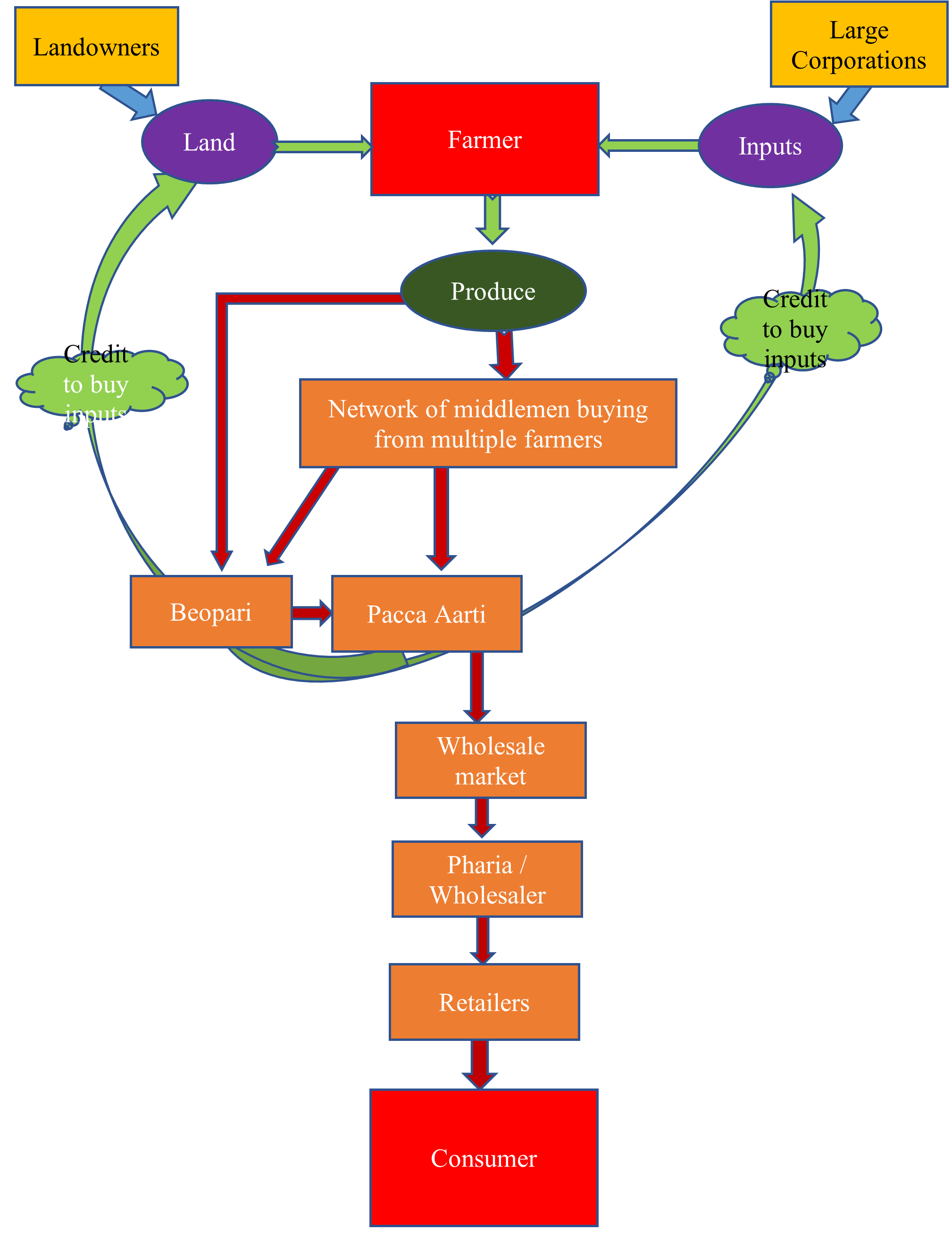

Fresh produce supply chains in Pakistan, like in other developing countries, are complex and involve a chain of agents from the farmer to the final consumer. These supply chains are intermediated through government-regulated fresh produce markets (FPMs), which serve as the primary link between producers and consumers of agricultural commodities in the country. FPMs are the physical locations where the majority of farmers deliver their produce personally or through a representative or a middleman for the purpose of auctioning/selling to other intermediaries, wholesalers, retailers, or end-users.

Figure 3 outlines a simplified flow of fresh produce supply chains for a typical small farmer in Pakistan. The supply chain starts with the farmer procuring inputs and land (if tenant). Since such farmers are typically credit-constrained, they rely on various agents to meet their liquidity needs. Once farmers produce the output, it is sold to one of these agents. These agents can be categorized as follow:

- A licensed Commission Agent, or ‘Paaca Aarti’ in local parlance, is an agent responsible for auctioning the produce in the government-regulated markets (called market committees).

- Non-Licensed Agent comprises ‘Kacha Aarti’ or ‘Beopari’.

- ‘Kacha Aarti’ is an agent who buys produce from small farmers and sells it to other middlemen or in the market.

- ‘Beopari’ is an agent who buys produce from farmers or other middlemen typically when the price is low and sells in the market when the price is high.

- After the produce is auctioned in the wholesale market, it is then sold by ‘Pharias’, who are agents that break the auctioned produce into smaller units to be sold to retailers.

- Retailers include big supermarkets as well as street vendors from where the consumers buy the produce.

Figure 3: Fresh produce supply chain for a typical small-scale farmer in Pakistan

Source: Authors' own primary data.

The authors’ ongoing research indicates that small liquidity-constrained farmers are dependent on these agents for credit, storage, transport, and marketing of the produce which they pay for indirectly by receiving lower prices from the respective agents. Farmers also frequently seek advice from these agents in choosing their agriculture practices. Due to the multifaceted role played by these intermediaries, interventions aimed at cutting out the middlemen may be counterproductive and therefore require more carefully designed interventions to improve farmers' and consumers' welfare.

What we need are marginal interventions specifically tailored towards increasing the performance of each segment of the supply chain. For example, there is a need to design formal credit products that meet the liquidity needs of (small) farmers given the perishable and bulky nature of fresh agricultural produce. This requires not only the design of a feasible product but also the promotion of trust between farmers and financial institutions. Other interventions need to focus on building the capacity of farmers to handle logistics and distributions of their output. Third, there is a need to improve access to markets for farmers and promote competition between middlemen. Finally, the introduction of agribusinesses that procure agricultural products directly from farmers is an encouraging development that will address some of the challenges of existing supply chains in the long run. In the short run, and before we can make a formal transition to e-markets, we must work towards fixing the traditional supply chains that serve the dietary needs of a majority of the Pakistani population.

Sher Afghan Asad is Assistant Professor of Economics, Lahore University of Management Sciences

Omar Hayat Gondal is Ph.D. Candidate of Economics, Washington University in Saint Louis

Mahbub ul Haq Research Centre at LUMS

Postal Address

LUMS

Sector U, DHA

Lahore Cantt, 54792, Pakistan

Office Hours

Mon. to Fri., 8:30 a.m. to 5:00 p.m.